April and May were a real swift kick in the teeth. There’s no hiding around the fact that the market wasn’t very nice to me or my trading accounts.

The vast majority of pairs in the portfolio blew out into major trends. That is bad news for a mean reversion strategy. When one currency trends, there are usually a handful bouncing around the mean. It gives us a chance to offset the losses. That didn’t happen recently, which is why my traders and I had a rough go of it.

I expect things to get better

Last month was bad enough that I completely ceased trading for two weeks. After turning the system back on in the second week of May, QB Pro continued to endure minor losses. That was thanks to one of the best trading decisions that I’ve made in the past year, which was to dramatically reduce the leverage.

The high risk account took a 6.2% loss. That would be very troublesome on a normal leverage account, but it’s a drop in the bucket by high risk standards. I look at it as more or less breaking even.

As a sign of my increased confidence, I increased my total deposits to $7,500 across the two accounts. As of today, the high risk account is back to trading on 20:1 leverage. It was at 5:1 for the past few weeks.

Changes to QB Pro

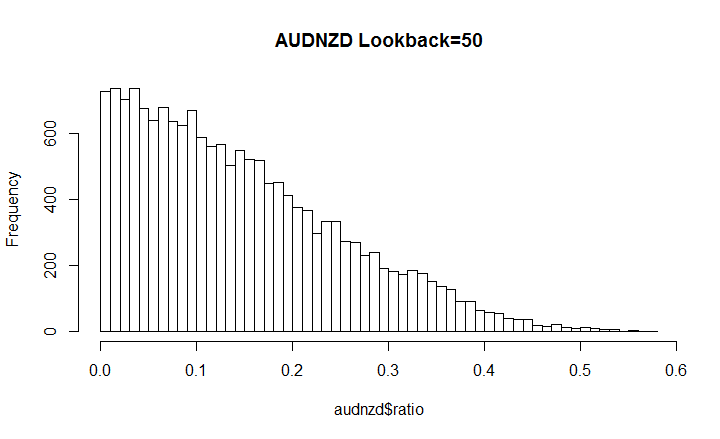

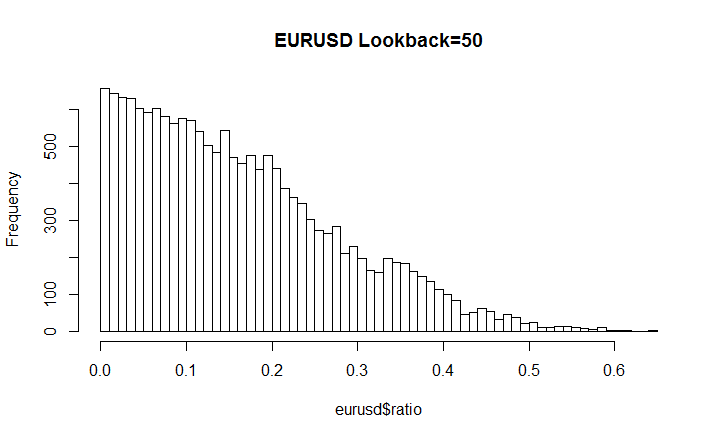

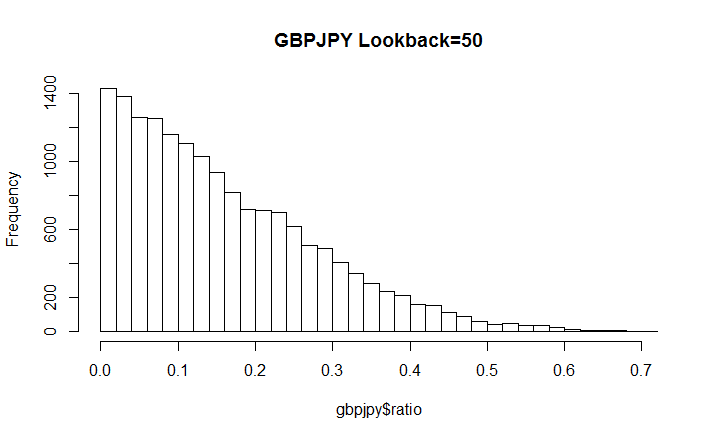

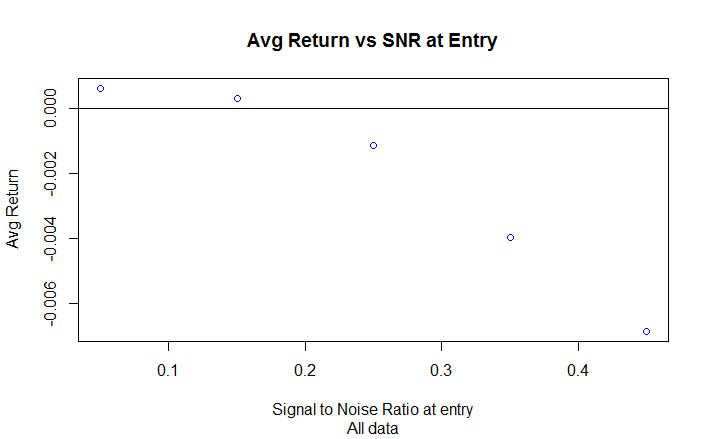

The signal to noise ratio contains enormous predictive power for my trades. I asked the question, “Does the signal to noise ratio at the time of entry predict the outcome of my QB Pro signals.

Judge for yourself.

The signal to noise ratio predicts the returns of QB Pro

The first two dots to the left represent 82.62% of all the QB Pro signals. That’s the reason that the strategy makes money.

I use 1/2π as the barrier between a range and trend. When the SNR < 1/2π, the profit factor is 1.5 (very profitable). When the SNR > 1/2π, the profit factor drops to an atrocious 0.62.

Conclusion: only take trades if the SNR is in the good area. That’s exactly what the updated strategy is doing as of last Friday.

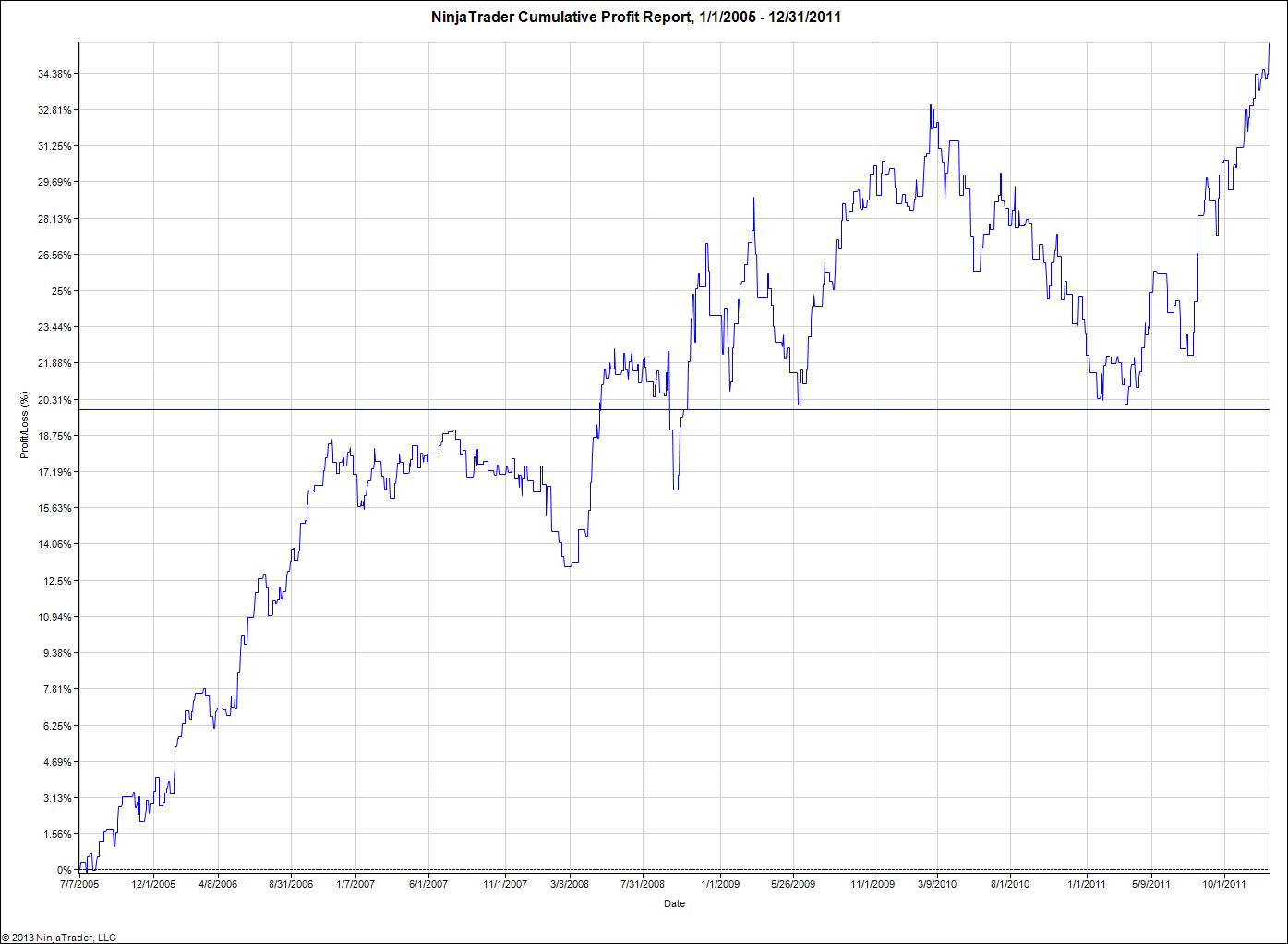

Based in part on experience and largely based on statistical analysis, I found a way to bend QB Pro into a historically profitable trending system on yen crosses. I’m sort of rushing this out the door because the market conditions are favorable. The accounts are trading USDJPY, EURJPY and GBPJPY on 1/3 of the overall portfolio. Perhaps I’m tapped out on the creativity front, but I’m calling this sub-strategy QB Yen.

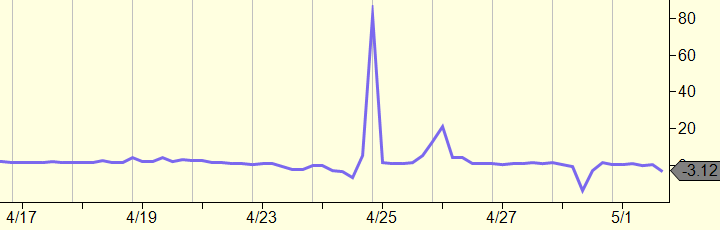

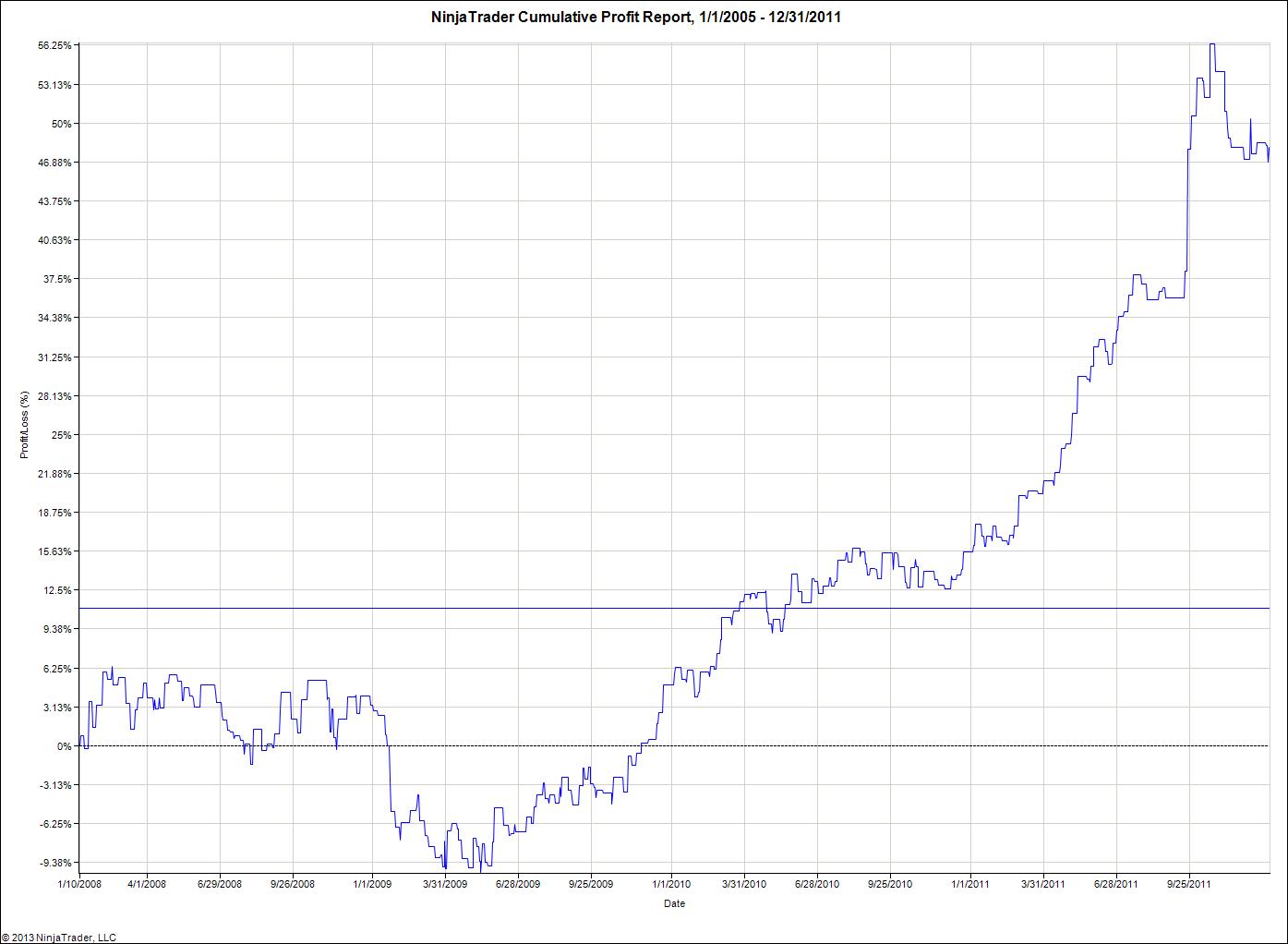

Here’s a screenshot of the equity curve for USDJPY in MetaTrader. This was part of my quality control analysis to ensure that the signals generated at the proper times.

I eventually want to analyze whether QB Yen can tolerate the spread costs of more exotic crosses like CADJPY. Until then, heavy weights will go on the most liquid yen crosses until it looks like they can handle the higher costs of the more exotic pairs.

QB Pro historically wins in 2 out of every 3 months. I don’t have enough data to judge whether consecutive losing months are dependent or independent, but it’s only happened twice historically where the system lost 3 months in a row. It’s never lost more than 3 consecutive months going all the way back to 2008.

Based on the new changes, the changing market conditions and the historical analysis of drawdowns, I feel much more comfortable putting more money into the account. For those of you that decided to take a break, I personally believe that the worst is over. The market will of course be the judge of that.